The EU’s new Corporate Sustainability Reporting Directive (CSRD) has brought the term double materiality into widespread use. But what does it mean to do sustainability reporting based on it, and how will the standardisation of sustainability reporting influence corporate strategies and goals?

Essential Themes of Sustainability

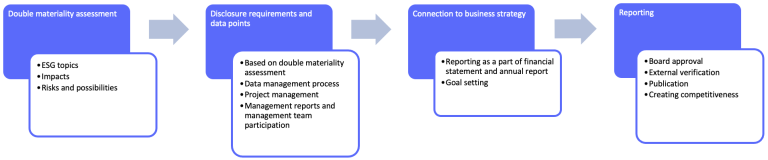

Corporate sustainability reporting from now on will follow the EU’s Corporate Sustainability Reporting Directive (CSRD). This directive introduces the principle of double materiality, which guides the process of materiality assessment. Double materiality identifies the key sustainability themes relevant to a company by considering the impact of the company’s operations on the surrounding world and the risks and opportunities the organisation should address within its business activities.

The directive is designed to align sustainability efforts across the European Union, supporting common goals such as combating climate change and promoting more sustainable energy consumption. Learn more about materiality assessments in our blog.

Sustainability Assessment and Minimum Disclosure Principles – Bureaucracy or Competitive Edge?

The directive enhances the overall understanding of sustainability practices across approximately 50,000 European companies, standardising the way sustainability is reported. This benefits not only customers and stakeholders but also the companies themselves. A standardised approach levels the playing field, making it easier to achieve competitive advantage through clear sustainability reporting.

It’s crucial not to approach materiality assessment merely for compliance – fulfilling the legal obligation without deeper engagement. Companies stand to gain far more from sustainability reporting and materiality assessments when they are genuinely invested in leveraging these themes to enhance their business strategy and ensure long-term resilience.

Managing the Reporting Process

Granite’s tools offer significant advantage in the data management phase of sustainability reporting. They streamline the process of gathering and organising information into a manageable format, enabling effective measurement and monitoring. Using spreadsheet software like Excel can make this process cumbersome and labor-intensive, especially when essential data is scattered and cannot be easily consolidated for comparison.

Granite’s tools provide a clearer overall picture, making it easier to report to leadership—an essential benefit when sustainability plans and actions must be integrated into the company’s business strategy based on the sustainability report. Since sustainability reporting forms part of a company’s financial statements, balance sheet, and board report, it plays a crucial role in setting future objectives.

It’s vital to involve company leadership throughout the sustainability reporting process, not just in presenting the final report to stakeholders. For many companies, sustainability reporting and double materiality assessments are entirely new concepts. The final report should be seen as a by-product of the process, with the primary goal being to enhance competitiveness and establish a robust foundation for adapting to regulatory changes at both national and international levels.

Granite’s tools provide a clearer overall picture, making it easier to report to leadership—an essential benefit when sustainability plans and actions must be integrated into the company’s business strategy based on the sustainability report. Since sustainability reporting forms part of a company’s financial statements, balance sheet, and board report, it plays a crucial role in setting future objectives.

Want to Elevate Your Organisation's ESG Profile?

Would you like to promote sustainable business practices while strengthening stakeholder trust? Explore the CSRD Sustainability Reporting Management Tool here.